- Free Rental Applications - 20+ Free Landlord Forms - Create Legal Documents in MInutes - Print Instantly - Download and Save - Created by Staff & Legal Professionals

The U.S. average asking rent rose $2 to $1,729 in July, but at a metro level is highly conditioned by supply expansion, according to Yardi Matrix.

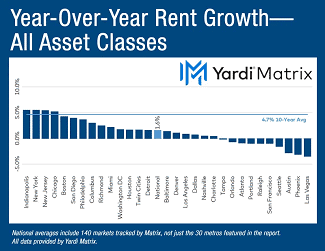

The U.S. multifamily market posted a solid performance in mid-2023, with asking rents in July advancing $2 to $1,729. Still, the growth rate remained on a moderating trend, up just 1.6 percent year-over-year—down 30 basis points from June and 400 basis points from the beginning of the year—according to Yardi Matrix’s latest survey of 140 markets. While Sun Belt metros returned to a more average rent performance, growth was led by markets in the Northeast and Midwest. Generally, rent growth is boosted by low supply expansion and high occupancy rates. Nationally, the occupancy rate remained flat at 95.0 percent for the fourth consecutive month and marks a 0.8 percent year-over-year decline. The SFR segment was also strong, with asking rents at $2,108 in July, up 1.2 percent year-over-year, and occupancy at 95.8 percent.

The job market also fueled demand in the multifamily sector, with the U.S. economy adding 1.7 million jobs in the first half of 2023. In addition, apartment absorption amounted to 120,000 units nationally, which, even though marks a decrease from the immediate post-pandemic levels, it is in line with historical norms. Year-over-year rent growth leaders were Indianapolis and New York (5.5 percent each), New Jersey (5.4 percent), Chicago (5.2 percent) and Boston (4.3 percent). Oppositely, rents fell in Las Vegas (-3.5 percent), Phoenix (-3.1 percent) and Austin (-2.8 percent). Supply growth influences rent growth—of the 12 metros in Matrix’s top 30 list with supply increases of 2.5 percent or more year-over-year, six posted negative rent growth, with Austin (4.4 percent stock increase year-over-year in July), Nashville (4.1 percent) and Raleigh (3.5 percent) in the lead. On the other side of the spectrum, Indianapolis and New York each had just 0.7 percent gains in stock.

Occupancy rates declined year-over-year through June in all but two of Matrix’s top 30 markets: Chicago (0.2 percent) and New York (0.1 percent). The largest decrease in occupancy was in Richmond-Tidewater (-1.8 percent); yet, the metro was among the top 10 metros for annual rent growth, up 2.5 percent.

Rent growth marked a 0.2 percent month-over-month uptick, led by Renter-by-Necessity rents (0.2 percent) while Lifestyle rents remained flat. RBN rents rose in 19 of the top 30 Matrix markets while Lifestyle rents rose in 13 markets. Philadelphia (0.9 percent), Chicago (0.7 percent), Tampa (0.6 percent), Denver (0.5 percent) and San Diego (0.5 percent) led in monthly gains. With nearly all deliveries adding to the Lifestyle segment, rents in the cohort decreased by 1.0 percent or more month-over-month in July in Orlando (-1.0 percent), Columbus (-1.1 percent) and Detroit (-1.8 percent). In Tampa, rents in the upscale segment rose 1.0 percent month-over-month.

Considering a 1031 Exchange?

Speak with the experts at 1031 Capital Solutions first.

National renewal rent growth rose 8.1 percent year-over-year in May. Although the rate is 40 basis points below April’s rate, it was three times higher than May’s asking rate (2.7 percent year-over-year). Miami (13.3 percent), Orlando (12.0 percent), Raleigh (10.7 percent) and Charlotte (10.5 percent) posted the highest rates. Moreover, renewal rents remained high in metros where the asking rent growth turned negative—Tampa (9.4 percent) and Seattle (8.2 percent). Meanwhile, national lease renewal rates declined from 64.4 percent in April to 59.4 percent in May. New Jersey (80.5 percent) remained the metro with the highest renewal rate, a consequence of the lack of available options, as occupancy rates were above 97 percent in Northern and Central New Jersey.

Demand for single-family rentals persists. Year-over-year asking rents rose 1.2 percent to $2,108 in July, while occupancy remained unchanged at 95.8 percent, a 0.4 percent year-over-year decline. The highest year-over-year rent growth through July occurred in Nashville (16.9 percent), Baltimore (12.5 percent) and Chicago (12.1 percent). Still, the SFR/BTR market continues to grow, and fast. Halfway through 2023, there were nearly 50,000 units under construction in communities with 50 or more units. Another 72,000 units were in the planning and permitting phases, according to Yardi Matrix.

Accessibility

Accessibility